Sending money to a stranger you will never meet, then staring at the screen while you wait for them to "release" the coins: almost everyone hesitates the first time, finger hovering over the confirm button. That caution is healthy, but it does not have to curdle into fear. Once you understand who is holding the crypto, whose hands your money passes through, and what the rule is at each step, P2P turns out to be a well-built system, and most of the dread comes from not knowing how it works. This guide walks the flow we have run ourselves many times, breaking picking a merchant, paying, receiving your USDT, and filing an appeal into separate stages, and it spells out the habits that actually keep your bank account out of trouble.

There is one prerequisite before you begin: a Binance account that has cleared identity verification. If you do not have one yet, you can open an account through this sign-up link, which carries the referral code BN03688 automatically and takes 20% off your trading fees (actual rate as shown on the Binance sign-up page). If registration or verification is where you are stuck, start with the Binance sign-up guide and the identity verification guide.

What is P2P, and is your money safe?

Here is the direct answer: P2P (also called C2C) is a marketplace where Binance matches you with an individual seller. You pay that person directly in your local currency, and Binance never handles your money. What it does instead is the one thing that matters most, from the second you place an order it locks the seller's USDT in escrow and only releases it to you once the trade is confirmed.

That escrow is the safety floor of the whole system. The scenario beginners fear most is "I sent the money and the seller denied getting it," and the answer is that the denial gets them nowhere. The moment your order is created, the matching amount of crypto in the seller's listing is frozen by the platform, out of the seller's reach too. As long as you hold genuine proof of payment, you open an appeal, Binance support checks it, and the escrowed crypto is force-released to you. In plain terms, on the buy side the odds of losing both your money and the coins are very low, provided you stay strictly inside the platform and let no one steer you off it.

Why does almost everyone buy USDT rather than Bitcoin directly? USDT is a stablecoin pegged to the US dollar, so its price barely moves. In the P2P market it carries the most listings, the tightest price competition, and the fastest fills. Buy USDT first, then take it to the spot market to swap for Bitcoin or any other coin: that is the standard route for most people, and the second half is covered in how to buy Bitcoin. For a more structured look at how P2P trading works under the hood, Binance Academy has solid beginner material to read alongside this.

The six steps from opening P2P to holding USDT

The flow is six steps: open the P2P entry, choose your coin and currency, pick a merchant, place the order, pay through the method the seller gave and tap "Transferred", then wait for release. When it goes smoothly, the whole thing takes under fifteen minutes from order to USDT in your account. Here it is broken out step by step.

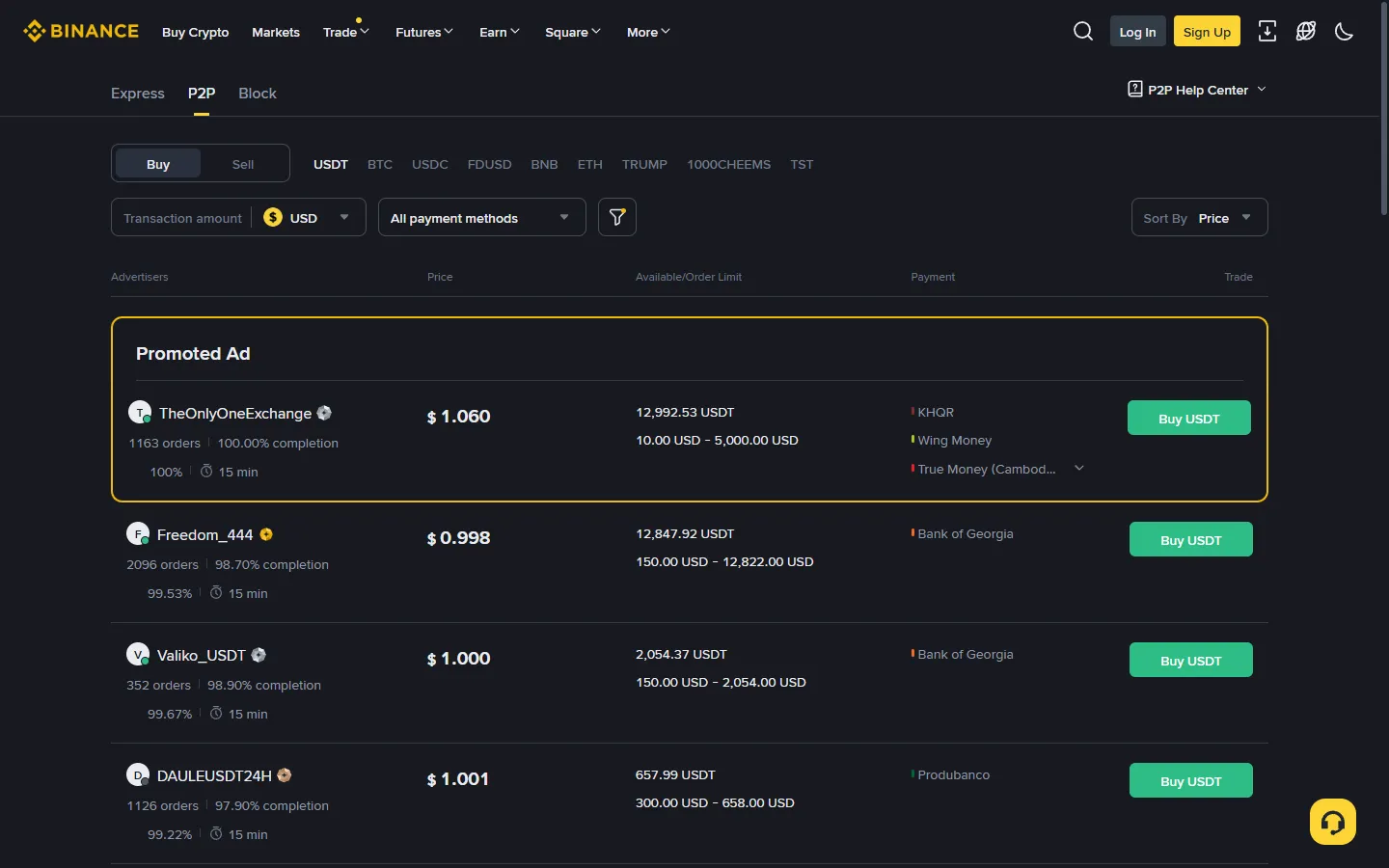

- Find the entry: on the app, tap "P2P" (or "Buy with P2P") on the home screen, or switch the Trade page to P2P; on the web it lives under the top "Buy Crypto" menu. Once inside, confirm you are on the "Buy" tab so you are facing the right direction.

- Choose coin and currency: set the coin to USDT and the fiat to whatever you hold, US dollars, euros, pounds, and so on. Type in the amount you plan to spend and the list filters down to listings that can fill it.

- Pick a merchant: do not just sort by price low to high and choose blindly. Order count, completion rate, and the verified badge matter far more than shaving a fraction off the price, and the next section covers how to read them.

- Place the order: open a listing, enter your amount, and confirm. The page starts a countdown, the seller's crypto is now in escrow, and you see the seller's payment details.

- Pay: open your own bank app or payment tool and send the money by the method shown on the order page. The amount must match the order to the cent, and leave the transfer note blank (the reason is below). Return to the order page and tap "Transferred".

- Wait for release: once the seller confirms the money landed, they release the USDT, it drops into your Funding wallet, you see the balance on the Assets page, and the trade is done.

One button needs a clear explanation: "Transferred" does not move any money for you. It is only a notice telling the seller "I have paid, please check." The actual transfer happens inside your own bank app. Tapping "Transferred" without having paid is a serious violation, the seller can report it, and your account takes a penalty.

A word more on payment methods: every listing marks which channels the merchant accepts, so before you order, confirm one of them is a method you can actually use. Listings that accept several methods give you more room if one channel suddenly will not go through. Each listing also has a minimum and maximum per order, and the amount you want to buy has to fall inside that band, which is exactly why entering your amount at the filtering stage screens out listings that cannot match.

On cost, P2P usually charges an ordinary buyer no fee at all. The merchant's margin is folded into the listed price, so the price you see is basically your entire cost (as shown on the page). That is one reason P2P tends to be cheaper than a card channel.

How to pick a merchant: four hard metrics

Judge a merchant on four hard metrics: order count, completion rate, the verified merchant badge, and how long the account has existed. When all four are solid, the chance of a trade going wrong drops sharply, and a cheap listing with ugly metrics is not worth touching however tempting the price.

| Metric | Where to find it | What to look for |

|---|---|---|

| Order count | The listing row and the merchant's profile, showing recent completed orders | The more the steadier; hundreds or thousands usually means a professional merchant |

| Completion rate | The percentage next to the merchant's name | Stick to 98% and above |

| Verified badge | The badge next to the name | Prefer verified merchants; they have posted a deposit with the platform and passed review |

| Account age | Registration and trading history on the profile | Skip brand-new accounts posting unusually low prices |

A note on price is worth making twice: a listing clearly below the market average almost always has a catch, either harsh conditions (an obscure required payment method, a demand for extra personal details) or an outright phishing attempt. The P2P market is competitive enough that ordinary merchants cluster into a narrow price band, so risking anything for a fraction of a percent on an oddly cheap listing does not pay.

If you have a minute, open the merchant's profile and skim the reviews, paying attention to the complaints. An occasional "slow to release" is tolerable; anything like "asked for extra money after I paid" or "tried to move me off the platform" is a hard pass.

One detail gets overlooked: below a listing there is usually a set of terms the merchant wrote, spelling out their requirements on the paying account and release timing, for example "payment only from an account in your own name" or "night orders released with a delay." Spending thirty seconds reading them heads off most after-the-fact disputes, because ordering without reading is treated, in an appeal, as accepting those terms. Our own habit: the clearer and more businesslike a merchant's terms, the more we trust them for repeat trades; a merchant who stuffs the terms with odd demands (say, a photo of you holding your ID) we skip no matter how good the price.

Three iron rules for the payment step

Hold three iron rules through the payment step, each one tied to the safety of your bank account: write nothing in the transfer note, pay only from an account in your own name, and never accept any form of third-party payment.

Rule one: no crypto words in the transfer note

"USDT," "Bitcoin," "crypto," "BTC," none of these belong in the transfer memo. In many countries, banks and payment processors run anti-fraud screening that flags this kind of keyword; at best the transfer is held or bounced, at worst your account gets a marker on it. The correct move is to leave the note blank. Some merchants call this out in their terms, and even when they do not, do it anyway; it protects you, not them.

Rule two: pay only from your own account

Binance P2P rules require the paying account's name to match your verified Binance identity. Pay from a spouse's or a friend's account and the merchant has every right to withhold release. This is not the merchant being difficult; it is a hard anti-money-laundering requirement, and in an appeal you would have no ground to stand on. The same holds later when you sell: receive money only into an account in your own name.

Rule three: no third-party payments

If someone offers "I will pay for you, you send me the coins," or asks you to buy coins on their behalf, refuse it however smooth the pitch. Third-party payment is a textbook fingerprint of money laundering and fraud-linked money movement, and getting tangled in it can mean a frozen account at best and helping with an investigation at worst. Your trade should only ever happen between you, the merchant, and the platform.

Beyond the three rules, your transfer amount has to match the order amount exactly. A cent over or under can trip up the merchant's automatic reconciliation and drag out the release for nothing.

Buying on P2P needs a verified account. Register with our referral code and get 20% off trading fees*. Enter it during sign-up, or tap the link below to carry it in automatically.

*Actual rate as shown on the Binance sign-up page and subject to change. See the affiliate disclosure.

What to do when a seller stalls on release

Take a breath first: the instant you placed the order, the seller's coins were locked in escrow, and they cannot vanish. If a seller sits on the release past the time limit, the appeal channel on the order page is available at any moment, and the final call rests with Binance.

Normally, release comes within a few minutes of your transfer, since professional merchants keep an eye on their accounts. If more than ten minutes pass with no movement, send a message in the order chat first with a screenshot of the successful transfer attached. Most of the time the seller simply had not noticed the incoming payment yet.

If the chat nudge goes nowhere and the order countdown is running down, tap the "Appeal" button on the order page and upload your proof of payment: the screenshot needs to show the amount, the time of transfer, and the recipient's details clearly. Once support steps in, they check with both sides, and confirming you really paid, they force-release the escrowed coins to you. Throughout the appeal the crypto stays locked, so no one can take it. For a knotty case, you can also file a ticket at the Binance support center.

There is one thing you must never do: cancel the order yourself after you have paid. Cancelling releases the escrow, the coins go back to the merchant, and your money is already gone; whether you get it back then depends entirely on the other person's goodwill, and you have handed over all your bargaining power. Commit this to memory: once you have paid, do not cancel the order no matter what the other side says.

The payment window and cancel rules

Every P2P order carries a payment countdown, commonly around fifteen minutes (merchants can set it differently, so go by the order page). If the countdown runs out before you tap "Transferred," the order cancels automatically and the escrowed coins return to the merchant.

A timeout cancel does not cost you money on its own, since you have not transferred anything. But frequency matters: cancelling several orders in a day (both manual cancels and timeouts count) gets you temporarily blocked from placing more that day. So before you order, make sure you have the time right now to finish the transfer, rather than placing an order and only then hunting for the right card.

The awkward case is when you have transferred the money but the order auto-cancels before you tap the button. If that happens, message the merchant on the order page immediately to explain, keep your proof of payment, and file an appeal if you need to. To avoid this bind, do not pay at the last second of the countdown; on a larger order, go and make the transfer the moment you place it.

Selling: the same logic in reverse

Selling USDT back to cash is the same machinery running in reverse: you post or take a listing on the P2P "Sell" tab, the platform holds your coins in escrow, the buyer transfers money to your account, and you release the coins only after you confirm the money truly landed.

Flip the direction and the risk flips too: buying, you worry the seller will not release; selling, the biggest trap is releasing before the money is really in your account. The iron rule is to go by the actual credit in your bank account. A transfer screenshot in the chat, or the buyer pressing "I have paid, release now," counts for nothing. Screenshots can be faked; a real settled credit does not lie.

Selling also carries a risk buying does not: the money you receive could itself be tainted. Freeze risk, safe receiving practice, and splitting into small amounts all deserve their own treatment, so we cover them in the Binance withdrawal guide. If cashing out is your plan, read that piece before you act.

The risks worth spelling out plainly

This section has to be blunt: P2P has real risks that escrow does not cover, and they sit mostly on the money side rather than the crypto side. Read this before you move any meaningful amount.

The one that surprises people most is your own bank. In many countries, banks and payment processors run anti-fraud monitoring that flags transfers linked to crypto exchanges or P2P activity. A sudden pattern of payments to unfamiliar individuals can trigger a temporary hold, a request to explain the source and purpose of the funds, or in some cases a frozen account while they investigate. This is a live reality across numerous jurisdictions, not a rare horror story, and it can hit you even when every transfer you made was legitimate. Splitting activity across time, keeping records, and not routing crypto trades through your primary salary or mortgage account all reduce the fallout.

The second is chargeback risk on reversible payment methods. Some rails, PayPal and certain card-based or instant-payment apps among them, let the payer reverse a completed payment. On P2P this cuts both ways. When you buy, expect many sellers to refuse reversible methods outright, precisely because a buyer could claw the payment back after the coins are released; you will usually be steered toward a plain bank transfer, which is non-reversible. When you later sell, treat any reversible incoming payment as unsettled until it has truly and irreversibly cleared, and prefer non-reversible rails where you have the choice. A payment that can be undone is not a payment you should release coins against.

The third is that the rules are local, and they vary enormously. Some countries require you to report and pay tax on crypto gains, some restrict or limit P2P trading specifically, some are fully permissive. Before you start, confirm the rules in your own jurisdiction and which services Binance offers where you live; the supported countries overview is a starting point, but your local regulator's guidance is the source of truth.

Our stance is out in the open: the point of this guide is to explain the mechanism clearly and help people who have decided to take part stumble less. It is not advice to participate. Whether you take part, and what consequences you carry, is your own call to weigh; see the disclaimer.

Frequently asked questions

How long does buying USDT on P2P take?

From the moment you finish the transfer to the seller releasing the coins, a few minutes is normal, since professional merchants watch their accounts closely. Add the time to pick a merchant, place the order, and pay, and the whole thing usually wraps up in about fifteen minutes. If a seller drags their feet on release, you can nudge them or open an appeal from the order page.

Are there fees to buy on P2P?

For an ordinary buyer, Binance P2P usually charges no trading fee. The cost is baked into the merchant's listed price, so what you see is essentially what you pay. A separate spot trading fee only appears later, when you take that USDT to the spot market to swap it for another coin.

If I pay and the seller never releases, could I lose the money?

The odds are very low. The instant you place the order, the matching amount of the seller's crypto is locked in escrow by the platform. As long as you hold genuine proof of payment, you open an appeal and support checks it, and the escrowed coins are force-released to you. The one rule: after you have paid, never cancel the order yourself, whatever anyone tells you.

Why do different merchants quote different USDT prices?

P2P prices are set by the merchants themselves and fold in each one's costs and margin, so listings differ slightly. A price noticeably below the market average usually hides extra conditions or is an outright trap, so it is not worth risking a fraction of a percent for a listing that looks too cheap.

First time using P2P, how much should I buy?

Run a small amount through the full loop first, buy, spot trade, withdraw, and confirm you can handle every step before you scale up. Digital asset prices swing hard, so at any point only put in money you can afford to lose.

A merchant wants me to move the chat to WhatsApp or Telegram. Is that OK?

No. A trade taken off the platform loses its escrow protection, is a common setting for fraud, and breaks the platform rules. Keep every message inside the order chat window, and treat anyone steering you to trade outside the app as a red flag to report.

The plain truth belongs at the end, as always: P2P only solves "how do I turn money into coins." Whether those coins then rise or fall is nobody's promise to make. Leaving the note blank, paying from your own account, and releasing only after the money lands protect your bank card; position sizing and a clear head about risk are what protect your capital. For anything this guide did not cover, write to [email protected], and we read and reply to everything.