Parking coins to collect interest sounds like the gentlest thing you can do in crypto, and I thought so too the first time. On my first run with Binance Simple Earn, I locked most of a position into a 90-day term for the sake of a fraction of a percent more yield. Halfway through, the market turned down. I watched the price slide with no way to redeem and no way to sell, and the interest I collected at maturity did not cover even a sliver of the paper loss. What this guide wants to spare you is the version of me that only stared at the yield number: operating Simple Earn is the easy part, and pricing the risks before you tap "Subscribe" is the real work.

A quick note on where you should be first. This article assumes you already have a verified Binance account with some idle coins sitting in it. If you have not opened an account yet, start with the Binance Sign-Up Guide; if you do not hold a single coin, the buying flow is in the P2P USDT buying guide.

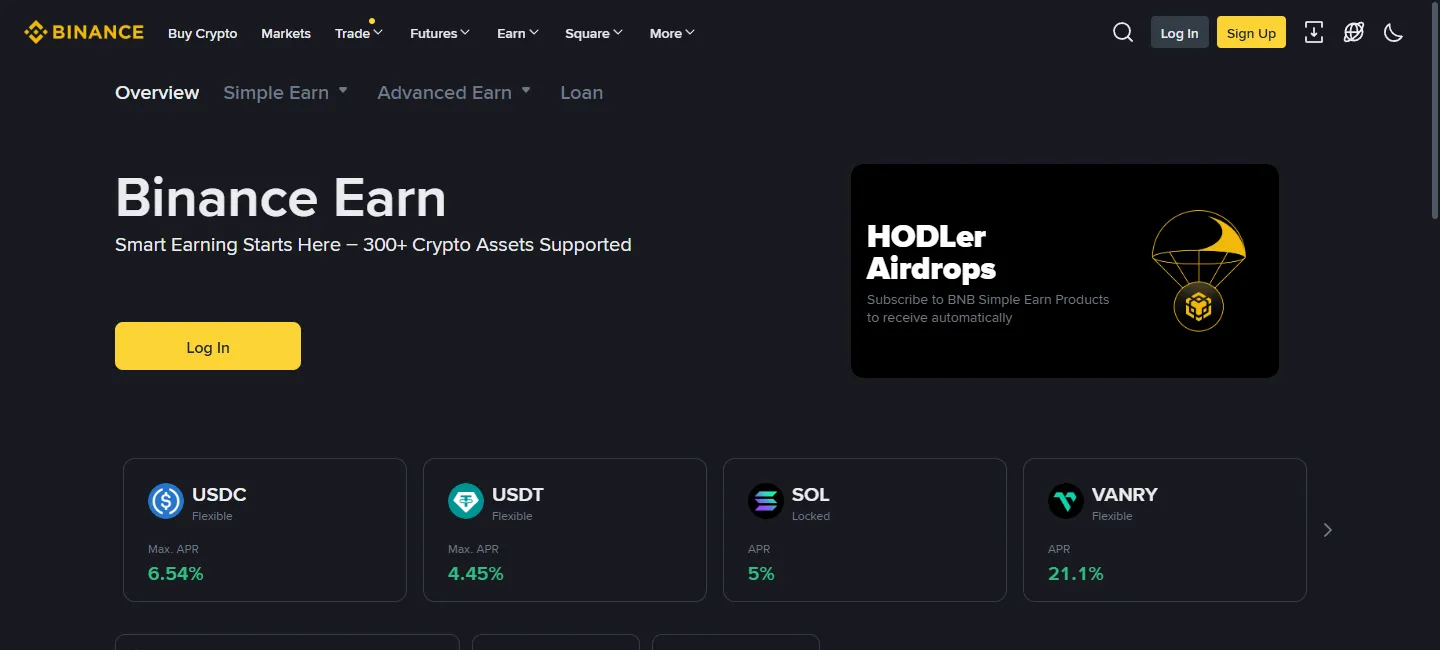

What is Simple Earn, and where do your coins go?

The short version: Simple Earn is Binance's product for putting coins you are not planning to touch to work, and it pays you interest for doing so. You subscribe idle coins into it, Binance directs those assets toward lending and similar activity on the platform, and a slice of what that earns comes back to you as interest, credited daily.

One analogy: it is a bit like moving a checking balance into a money-market fund. The coins are the same coins; they simply shift from sitting in your Spot wallet to being lent out. But the analogy only helps with the shape of the thing, not the risk. A money-market fund sits on treasury bills and bank paper, while Simple Earn sits on borrowing demand in the crypto market, and the two are not in the same risk league. The risk section below does the actual accounting.

The barrier to entry is low: for major coins a few dollars' worth is often enough to start, hundreds of coins are supported, and which coins you can subscribe and at what rate is all visible on the Earn page in the app. Readers who want the mechanics from the source can search Simple Earn on Binance Academy.

Flexible vs Locked: which one should you pick?

Here is the verdict up front: Flexible lets you subscribe and redeem at will and pays a lower rate; Locked ties your coins up for a set term at a higher rate, but redeeming early forfeits the rewards already accrued. The whole difference lives in one trade-off, flexibility against rate.

| Point | Flexible | Locked |

|---|---|---|

| Access | Subscribe and redeem anytime; redemption usually lands fast | Fixed lock term, commonly tiers from a few dozen to over a hundred days |

| Rate | Lower, floating with market supply and demand | Usually higher than Flexible for the same coin |

| Early redemption | No such concept; redeem whenever | Principal can be pulled early, but accrued rewards are forfeited |

| Reward payout | Accrues daily, paid daily | Accrues daily; payout rhythm per the product page |

| Best for | Coins you might need to move at any time | Coins you are sure you will not touch |

Which should you pick? Our steer is conservative: as a beginner, stick to Flexible only. The extra yield on Locked is bought with "you cannot move the position when the market lurches", and lurching is the one thing the crypto market never runs short of. Once you have lived through a full up-and-down cycle and know which coins you can actually hold through it, then think about placing a portion of your genuinely untouchable coins into Locked.

What does the APR shown on the page actually mean?

That percentage is an annualized rate. It answers "roughly how much would this pay if I held it for a full year at this rate", not "you have locked in this return by subscribing". Reading it correctly comes down to three points: it is annualized, it accrues daily, and it floats at any time.

A quick illustration makes it click. Say a coin's Flexible APR shows 5% (an illustration only; real rates float and the Binance page shows the live figure), and you subscribe the equivalent of 1,000 USDT for 30 days. The interest is roughly 1,000 × 5% ÷ 365 × 30 ≈ 4.1 USDT. Five percent a year sounds like plenty; spread across a month it is a little over four dollars, and that gap is where a lot of first-timers feel let down when they check.

Two more details. One, many coins tier the Flexible rate: a small first slice earns the higher rate, and anything above it drops sharply, so read the tier rules before subscribing a large amount. Two, the rate is not a promise; today it is one number and next week it may be another, especially the "bonus rate" or "limited-time rate" that stands out well above its peers, which usually carries time and size caps. At all times go by the live figure on your own page. Any rate written down by a third party, this article included, will go stale.

How do you subscribe and redeem?

The operation is not hard: four steps to subscribe, three to redeem, all inside the app. Using Flexible as the example, subscribing looks like this:

- Open the Binance app, find "Earn" on the home screen (or search Simple Earn), and enter the product list;

- Pick the coin you want to subscribe, tap in, and check the rate, the type (Flexible or Locked), and the tier rules;

- Enter the amount; the system shows an estimated daily reward, and once it looks right, submit;

- Return to the Earn account page and confirm the assets have moved from your Spot wallet into the Earn position.

Redeeming is the reverse:

- Go to the Earn account, find the position you want to redeem, and tap "Redeem";

- Enter the amount; Flexible usually offers a fast redemption, with the arrival time shown on the page;

- Confirm, then check your Spot wallet; from there, sell or transfer as you like, with the cash-out flow in Withdraw & Cash Out.

The Locked subscription flow is the same, with one extra step to choose the lock term. When you redeem before maturity, the screen states plainly how much reward you will forfeit, so read it before you confirm. Subscribing and redeeming themselves are free, but when you convert the interest into another coin or withdraw it, the normal trading and withdrawal fees still apply, detailed in Fees Explained.

Register on Binance with our referral code and get 20% off trading fees*. Simple Earn is ready to use as soon as your account is verified.

*Actual rate as shown on the Binance sign-up page and subject to change. See the affiliate disclosure.

What are the risks of Simple Earn? Price these in first

The most important sentence goes at the top of this section: Simple Earn is not a bank deposit, it is not covered by deposit insurance, and your principal can lose value. Its risks also rank in an order that runs against most people's intuition. The thing to worry about most is not whether the interest gets paid; it is the three accounts below.

The first account: price swings dwarf the interest

This is the account most easily hidden behind the yield number. Say you subscribe the equivalent of 10,000 in local currency of BNB into a 120-day Locked term at a 3% APR (an illustration; rates float and the Binance page shows the live figure). The interest at maturity works out to roughly 10,000 × 3% ÷ 365 × 120 ≈ 98. Now suppose that over those 120 days BNB falls 20%, which in the crypto market is an ordinary move: your principal is down 2,000 on paper, and the interest covers about one twentieth of it.

Put another way, the interest earns you the digits after the decimal point, while the coin's price moves the digits in front of it. Subscribing to Earn does not change the fact that you carry the coin's price risk; it lays a thin layer of interest on top of that risk. Before you decide whether to subscribe, answer the bigger question first: this coin itself, are you willing to hold it for that long?

The second account: platform risk

Coins sitting in an Earn position mean the actual control of the assets is in the platform's hands. If the platform hits trouble in its operations, gets hacked, or has activity frozen by regulators, your assets can be caught up in it. This is not scaremongering: the collapse of FTX turned "even a big platform can blow up" into common sense that every coin holder should keep front of mind. Binance's scale and risk controls sit near the top of the industry, but "near the top" and "zero risk" are an ocean apart. The response is plain too: do not stake your net worth on any single platform, consider a self-custody wallet for large long-term holdings, and for an analysis of the platform's own safety, read Is Binance Safe?.

The third account: the opportunity cost of locking

During a Locked term you cannot cut a losing position; redeeming early forfeits rewards and may still make you wait. If the coin rises and you want to take profit, you again have to go through redemption first. When the market moves hard, the loss from being unable to act can far exceed the interest earned. There is a quieter trap too: subscribing stablecoins feels like it carries no price risk, but stablecoins themselves have depegged before. The odds and the size are relatively small, which is not the same as zero.

Why does a promised, can't-lose yield deserve suspicion?

Here is the test to apply: Binance's official pages always describe returns as "estimated" and "floating", and never promise a floor under them. Anyone making you a cast-iron promise is running either a fake page or a scam, with no third option.

The common scripts go like this. Someone in a chat group posts an "internal Earn channel, locked-in 30% a year" and asks you to move coins to a specified address. A fake app displays absurdly high rates, and once you top it up you can never withdraw. Someone posing as official support messages you first, coaching you to "upgrade your account for higher interest". What these share is steering you off official channels to move coins. One line covers it: real Binance Simple Earn only happens inside the official app and website, and your coins never need to be sent to any personal address. When something feels off, verify it first at the Binance official support center, and see more of these tactics pulled apart in Scam Prevention.

There is also a situation that is not a scam but still deserves a wary eye: genuine high-APR promotions on new coins. The number is real, but it is usually capped by time and size, and the new coin's own price swings so hard that even a high APR can lose to the price falling. When you see a high rate, ask first "why is this so high", and the answer is usually written in the fine print of the promotion terms.

Who is Simple Earn a good fit for, and who is it not?

One-line profile: people who already plan to hold a coin for the long term, whose coins are going to sit in the account anyway, are well suited to parking them in Flexible for a bit of interest; people counting on Earn interest to make them wealthy are not. To spell it out:

- Good fit: long-term holders. Coins sit idle in the Spot wallet either way, and moving them into Flexible at least earns interest, redeemable whenever you need them;

- Good fit: dollar-cost-averaging buyers. Move the coins you accumulate into Flexible, and use the DCA Cost Calculator to keep your cost clear;

- Poor fit: short-term traders. Subscribe and redeem carry a time lag, so when the market moves you cannot act, and you trip over a dollar to pick up a dime;

- Poor fit: anyone treating it as a bank deposit substitute. It has no deposit insurance and the principal rises and falls with the coin price, an entirely different thing;

- Poor fit: anyone buying a coin specifically to chase a high APR. Buying an asset you did not otherwise want, just for the interest, has the logic backwards.

If you happen to hold BNB, it is worth getting to know Launchpool Farming too. It is also about putting coins in to earn, but the source of the reward and the risk structure differ a lot from Simple Earn. Readers who want exposure to US stocks can look at bStocks Tokenized Stocks. Knowing more tools does no harm, but each extra one you use means one more risk account to run.

Frequently asked questions

Can Simple Earn lose my principal?

It can. The most common way to lose money is the coin you subscribed falling in price: you redeem the same number of coins, but they are worth less in cash terms. Beyond that, there is platform risk in extreme cases. Simple Earn is not a bank deposit and carries no deposit insurance, so treat any claim that your principal is perfectly safe as a red flag.

Can I withdraw Flexible savings at any time?

Usually yes. Flexible products support redemption at any time and the coins typically arrive quickly, with the exact timing shown on the redemption screen. In rare extreme markets a platform may temporarily throttle some functions, so do not treat redeem anytime as an absolute promise, and keep emergency money out of it.

Can I redeem a Locked product before it matures?

Yes, you can get your principal back, but the cost is that the rewards already accrued on that subscription are forfeited, and in some cases redemption still takes a short wait. If you might need the money during the term, choosing Flexible from the start saves the headache.

When are rewards paid, and where do they land?

Rewards usually accrue daily and are paid daily, with Flexible rewards typically credited in the same coin you subscribed, to your Earn or Spot wallet. Start times and payout rhythm vary by product, so go by the notes shown on the page when you subscribe.

What is the difference between Simple Earn and Launchpool?

Simple Earn pays interest in the coin you subscribed, and the amount is relatively predictable. Launchpool pays you a new project's token, whose value depends on the coin's price after listing, which cannot be worked out in advance. Both leave you exposed to the price swings of whatever coin you put in.

To wrap up: "earn" sounds settled, but dropped into the crypto market it is never steadier than the coin's price itself. Treat Simple Earn as a handy optimization on a long-term holding rather than a money-making tool, and your frame of mind is in the right place. For anything this guide did not cover, write to [email protected], and we read and reply to everything.